Most estimating organisations would agree, in principle, that learning from actuals should be straightforward. Projects are delivered, costs are recorded, and the differences between estimated and actual outcomes ought to feed directly into better future estimates. In practice, that feedback loop is weak at best, and in many cases effectively broken.

This is not due to a lack of intent. Estimators generally want better access to actuals, and project teams are usually willing to share what they have. The difficulty lies in turning delivery data, which is created for commercial control and reporting purposes, into analytical input that meaningfully improves estimating performance. That transformation is far more complex than it appears, and the challenges are as much organizational as they are technical.

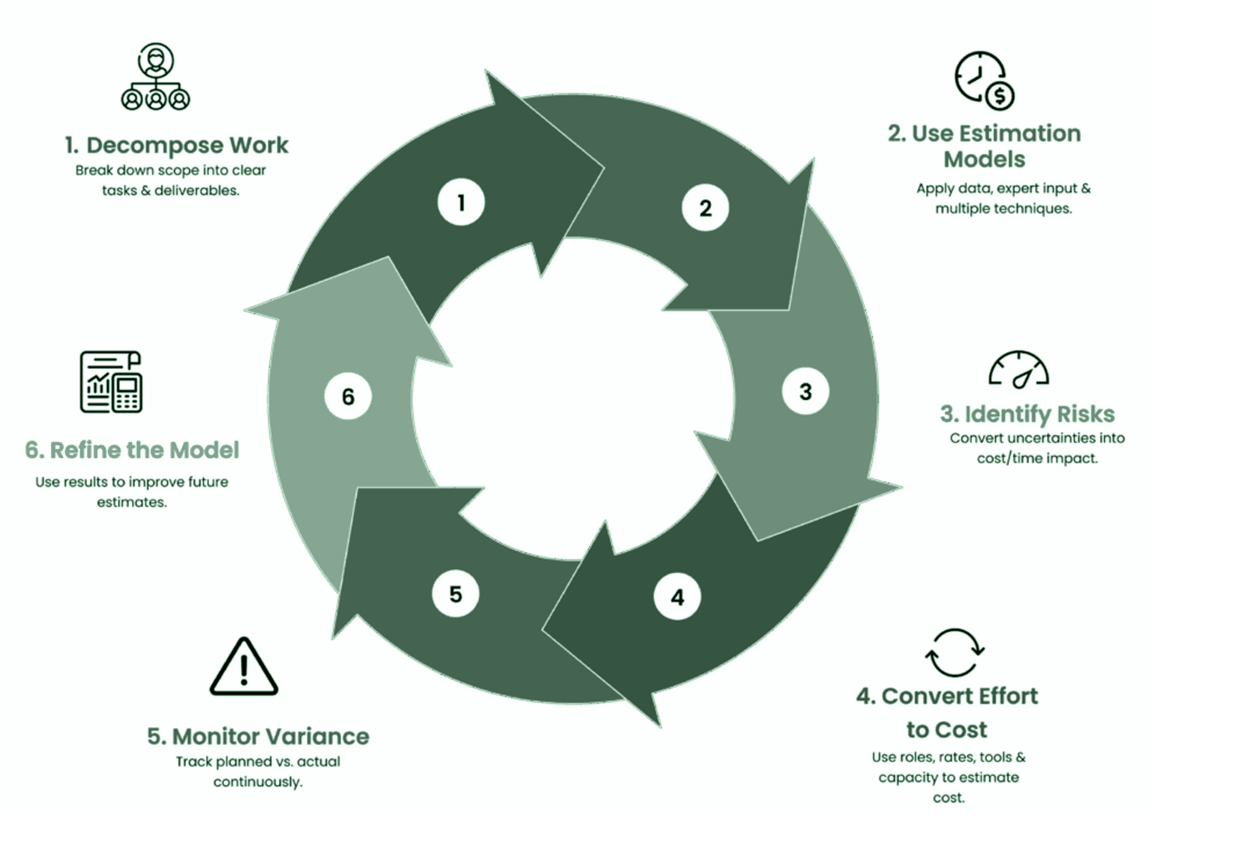

Why "Use Your Actuals" Is Easier Said Than Done

Actual cost data is collected to answer a different set of questions than those estimators are trying to solve. Accounting systems are designed around financial control, compliance, and reporting. Estimating, by contrast, is concerned with understanding how cost behaves as scope, context, and delivery approach change.

This mismatch shows up immediately when estimators attempt to reuse delivery data. Costs are captured at the wrong level of granularity. Scope is implicit rather than explicit. Key drivers that matter during estimating (physical characteristics, site constraints, delivery choices) are often absent or embedded in free text fields that resist systematic analysis.

Even when actuals are available, they are rarely aligned with the way estimates were originally constructed. Cost codes evolve during delivery as project teams respond to practical realities. Work packages are split, combined, or reclassified. Changes are approved for commercial reasons that do not map cleanly back to estimating assumptions. By the time the project closes, reconstructing a clean comparison between "what we thought would happen" and "what actually happened" becomes a forensic exercise requiring more effort than most organizations can sustain.

The result is that many organisations fall back on anecdotal learning. Lessons are discussed informally, often without a persistent record, and the same estimating debates recur project after project. The feedback loop exists in theory but fails in practice because the infrastructure to support it systematically is missing.

The Timing Problem: When to Capture Actuals

One of the most underappreciated challenges is timing.

Final account settlements often occur twelve to twenty-four months after practical completion. By that point, the project team has dispersed, institutional memory has faded, and the estimating context has moved on. Key personnel who could explain why certain costs emerged as they did are working on different projects or have left the organization entirely.

Waiting for final accounts before learning from actuals means accepting a feedback loop that operates on a three to four year cycle including project duration. For organizations delivering similar assets repeatedly, this delay is strategically problematic. Estimates for the next wave of projects are prepared using assumptions that could have been updated but were not because the learning process lagged too far behind.

The alternative is capturing intermediate actuals at defined project milestones (design freeze, construction midpoint, substantial completion) in addition to final accounts. This compresses the feedback cycle but introduces different challenges. Intermediate costs are provisional. Scope may still be incomplete. Risk allowances have been partially consumed but final allocation is unknown. Despite these limitations, organizations that successfully learn from actuals often find that timely but imperfect data is more useful than delayed comprehensive data, provided the analytical methods can accommodate uncertainty.

This creates a practical question with no universal answer: at what point in the project lifecycle should actuals be captured for estimating purposes? You have to pick based on your organizations data an needs, but avoiding the question guarantees that learning remains perpetually deferred.

The Distinction Between Reconciliation and Learning

One of the most common pitfalls is treating post-project reconciliation as the same thing as learning from actuals. Reconciliation answers the question: where did the money go? Learning asks a different question: what does this tell us about cost behaviour under different conditions?

Reconciliation tends to focus on variance at a project level, whether the project finished over or under budget and why. That information is useful for commercial purposes and for understanding delivery performance, but it does not automatically translate into improved estimating capability. Learning requires actuals to be decomposed in a way that aligns with estimating logic rather than accounting structure.

For example, knowing that a project overran due to "ground conditions" is not sufficient for estimating purposes. Estimators need to understand how ground conditions were characterised at estimate time, how they actually manifested during delivery, which scope elements were affected, and how sensitive cost was to those conditions relative to other drivers. Without that structured understanding, lessons remain qualitative and difficult to apply consistently when estimating the next project.

The distinction matters because it determines what data needs to be captured and how it needs to be structured. Reconciliation can function adequately with financial reporting categories. Learning cannot.

Mapping Actuals Back to Estimating Assumptions

Closing the loop between estimates and actuals requires a deliberate mapping between estimating assumptions and delivery outcomes. This mapping is rarely available by default because the two activities operate in different systems with different purposes.

At estimate time, assumptions are often implicit. Productivity rates are selected based on experience but not documented explicitly. Contingencies are applied at a summary level without specifying what risks they are intended to cover. Delivery methods are assumed rather than stated. If these assumptions are not recorded in structured form, there is nothing concrete to test when actuals become available.

One practical step is to treat estimating assumptions as data, not narrative. Key drivers, scope boundaries, and contextual factors should be captured in structured fields at estimate creation, even if they are uncertain at that stage. This does not require perfect accuracy; it requires consistency. A structured assumption record for a roadworks project might include fields for: pavement thickness, base material type, traffic management approach, possession constraints, proximity to services, ground conditions assessment, and assumed productivity bands for key activities. Each field would contain the assumption made at estimate time, providing a baseline for comparison when actuals emerge.

On the delivery side, costs need to be associated with those same drivers. This does not mean reconfiguring accounting systems wholesale, but it does mean introducing a translation layer that maps financial cost codes to estimating drivers. This translation is often imperfect and requires judgment about how to allocate costs that span multiple categories, but it enables systematic analysis across projects rather than project-by-project manual interpretation.

This translation step is where many initiatives stall, because it sits between estimating, project controls, and finance functions. It therefore belongs to no one by default, and without explicit ownership and resourcing, it does not happen consistently enough to support learning.

Dealing with Partial and Imperfect Actuals

Even with good intent and adequate resourcing, actuals will never be complete or perfectly clean. Projects are interrupted. Scope changes mid-stream. Cost attribution is approximate. External factors introduce noise that cannot be fully disentangled. Attempting to wait for "clean" data before learning from actuals is usually an excuse for inaction that perpetuates the status quo.

The more productive approach is to accept imperfection and design analytical methods that can tolerate it. This is where modern statistical and machine learning techniques offer practical value beyond traditional post-project review methods.

Rather than requiring every project to have a complete set of attributes, models can be designed to learn from partial observations. Projects contribute information where they are comparable and are excluded from specific analyses where they are not, without being discarded entirely. This is conceptually different from forcing all data into a single uniform structure or limiting analysis only to projects that meet stringent completeness criteria.

For example, consider a utility organization with cost data across multiple pipeline projects. Historical records might show good consistency for pipe diameter, length, and material across the full portfolio, but inconsistent or missing information for ground conditions, traffic management approach, or utility conflicts. Analytical models can still learn robust relationships for the well-recorded drivers while treating other factors probabilistically rather than deterministically, gradually incorporating them as data coverage improves. This incremental approach allows learning to begin with available data rather than waiting for an idealized dataset that may never materialize.

Driver-Level Learning: The Critical Shift

One of the most important conceptual shifts when using actuals effectively is moving away from project-level learning toward driver-level learning. This shift is fundamental to making actuals useful for estimating rather than merely for retrospective accounting.

Projects are unique combinations of many factors. When outcomes are analysed only at a project level, it becomes difficult to disentangle which factors actually drove cost differences and which were incidental. Driver-level analysis, by contrast, asks how cost responds to changes in individual inputs while controlling for others, isolating the relationships that matter for estimating.

This approach aligns naturally with parametric estimating. Each completed project becomes a set of observations about how specific drivers behaved under particular conditions. Over time, patterns emerge that are difficult or impossible to see when projects are treated as indivisible wholes that can only be compared in aggregate.

Consider the types of questions that driver-level analysis can address systematically:

How does unit cost change as pipe diameter increases, once installation method and ground conditions are accounted for?

How sensitive are earthworks costs to haul distance relative to volume, and at what distance does haul become the dominant cost component?

At what point do site access constraints begin to dominate labour productivity, and how does that relationship differ across asset types?

These are estimating questions, not accounting ones, and they require actuals to be structured to support this type of decomposition. The answers are unlikely to emerge from narrative lessons learned reports, but they can emerge from systematic analysis of actuals structured around estimating drivers.

A Conceptual Example: Productivity Learning

To make driver-level learning more concrete, consider a conceptual example of how actuals might inform productivity assumptions, a persistent challenge in construction estimating.

Imagine a contractor delivering multiple similar civil assets across different sites. Productivity varies significantly between projects, and post-project reviews typically attribute this variation to "site conditions" in general terms without systematic analysis. This provides little useful guidance for future estimates beyond a general sense that productivity assumptions should be conservative.

By mapping actual labour hours back to a consistent set of measurable drivers (site access configuration, working space constraints, asset complexity, local labour market conditions, and weather impact), patterns that were previously obscured can become visible. Analysis might reveal, for instance, that certain access constraints consistently reduce productivity by twenty to thirty percent beyond what was assumed at estimate time, while other constraints that estimators worried about matter less than expected. Weather delays might prove to be less correlated with rainfall totals than with the number of discrete weather interruptions, changing how weather allowances should be estimated.

This type of insight can be fed directly back into estimating practice. Productivity assumptions are adjusted based on evidence rather than anecdote. Contingency is redistributed toward genuinely volatile drivers rather than spread uniformly. Early-stage estimates become more defensible because they are grounded in observed relationships rather than generic industry rules that may not reflect the organization's actual delivery context.

The key is that learning occurs at the driver level, supported by structured data rather than by informal recollection of what happened on previous projects. This does not eliminate uncertainty, but it makes uncertainty more honest and better calibrated to organizational experience.

The Role of Statistical and ML Techniques

Traditional post-project reviews rely heavily on manual analysis and expert interpretation. While valuable, this approach does not scale well across large portfolios and struggles to extract systematic patterns from noisy data. Statistical and machine learning techniques offer a way to systematise learning without discarding professional judgement.

Regression analysis remains a useful baseline. When applied thoughtfully, it can quantify relationships between drivers and cost outcomes, highlight outliers that merit investigation, and test the stability of assumptions across different contexts. However, regression alone struggles when data is sparse, noisy, or exhibits high collinearity among drivers, all of which are common conditions in construction datasets.

Modern analytical approaches address these limitations in several practically useful ways:

Regularisation techniques (ridge regression, LASSO, elastic net) explicitly penalize model complexity, discouraging the fitting of relationships that are not strongly supported by the available data. In the context of learning from actuals, this produces more conservative behaviour that is less prone to overfitting when sample sizes are limited. Rather than chasing every fluctuation in observed costs, regularized models identify the drivers that consistently matter across multiple projects.

Bayesian methods allow prior estimating knowledge to be combined explicitly with observed actuals rather than being overridden by limited data. This is particularly valuable when organizations have strong domain expertise but relatively few completed projects in a specific context. For example, an organization with decades of experience delivering pump stations but only five completed projects in the past three years can use Bayesian updating to weight that accumulated knowledge appropriately rather than letting five recent observations dominate. As additional projects complete, the model updates its understanding incrementally and transparently.

Hierarchical models support learning at multiple levels simultaneously, for example across an entire portfolio, within specific asset types, and at the individual project level. This structure mirrors how estimators actually think about transferring knowledge. Insights that apply broadly across all projects can be distinguished from those that are specific to particular contexts, and both types of information are used appropriately when estimating new work.

Non-linear and interaction effects can be identified systematically rather than requiring manual specification. Machine learning models can detect threshold effects (for example, site constraints that matter only above a certain severity) and interactions between drivers (for example, how ground conditions affect productivity differently depending on access constraints) that are difficult to reason about explicitly in advance.

Importantly, these techniques are most valuable when paired with explainability methods that make model behavior transparent. Estimators need to understand why models behave as they do, not just what they predict. Sensitivity analysis, driver importance measures, and partial dependence plots support that understanding and help identify when models are behaving in ways that contradict domain knowledge and therefore require investigation.

Defining Success: What Should Actually Improve?

Organizations implementing actuals-learning programs often fail to define success clearly, making it difficult to assess progress or justify continued investment. Learning from actuals should improve specific, measurable aspects of estimating performance, not merely create activity.

Potential success metrics include:

Improved calibration of uncertainty: Are confidence intervals around estimates well-calibrated, meaning that actual costs fall within stated ranges at the expected frequency? A model that is wrong fifty percent of the time but correctly represents uncertainty is often more useful than one that appears accurate on average but systematically under-represents risk.

Reduced variance in estimate-to-actual performance: Are subsequent estimates converging more tightly around actual outcomes, even if bias remains? Reduced variance suggests that random noise is being filtered from systematic patterns.

Better risk allocation: Are contingencies being consumed more predictably, with fewer large surprises? This suggests that risk drivers are being identified and quantified more accurately.

Faster convergence as design matures: As projects progress from concept to detailed design, estimates should converge toward eventual outcomes. Are subsequent estimates converging faster and more smoothly than historical patterns?

Increased consistency across estimators: Are different estimators producing more similar results for comparable work? This suggests that learning is being embedded in systematic methods rather than remaining tacit knowledge held by individuals.

Success should be defined before implementation begins, and metrics should be reviewed periodically as the program matures. Without clear metrics, actuals-learning programs risk becoming permanent initiatives that consume resources without demonstrating value.

Ownership and Governance: Where Implementation Actually Fails

Technical capability is necessary but insufficient. Most actuals-learning programs fail because of organizational and governance issues rather than analytical limitations.

Ownership remains the primary challenge. Learning from actuals sits at the intersection of estimating, project controls, and finance, and therefore belongs fully to none of them. Estimating teams want access to actuals but typically lack authority over delivery data collection. Project controls teams own the data but may not understand estimating needs. Finance teams maintain the systems but are focused on compliance rather than analytical use.

Without explicit ownership and clear authority, the translation layer between financial reporting and estimating analytics does not get built or maintained. Responsibility for data quality becomes diffuse, and when learning from actuals competes with other priorities, it consistently loses.

Successful implementations typically establish a dedicated cost intelligence function or embed clear responsibility within the estimating team with explicit collaboration protocols across functions. This function owns the analytical logic, defines data requirements, performs the translation between accounting and estimating structures, and is accountable for demonstrating that learning is improving estimating performance.

Funding and prioritization present related challenges. Building the infrastructure to learn from actuals requires upfront investment in data engineering, analytical capability, and process change, with benefits that are diffuse and emerge gradually over multiple project cycles. This profile makes it difficult to justify within typical project budgeting frameworks.

Organizations that succeed typically frame this as strategic investment in estimating capability rather than as project-specific cost. The benefits accrue across the portfolio and compound over time as more actuals are incorporated, but this requires leadership commitment to fund development before tangible returns are visible.

Integration with existing systems determines practical adoption. If learning from actuals requires estimators to adopt entirely new tools or workflows, resistance is predictable. More successful approaches layer analytical capability on top of existing estimating processes, making insights available within familiar interfaces rather than requiring wholesale system replacement.

Framing matters culturally. If actuals are perceived as being used primarily to audit or criticize past estimates, data quality deteriorates rapidly as both estimators and project teams become defensive. Learning from actuals must be framed explicitly and consistently as improvement rather than judgment. The goal is better future estimates, not retroactive criticism of past ones. Organizations that maintain this framing clearly and protect it operationally achieve better data quality and estimator engagement.

Implementation Maturity: A Practical Path Forward

Organizations are at different starting points in their capability to learn from actuals. Rather than attempting to implement sophisticated analytical frameworks immediately, a more realistic approach recognizes maturity levels and builds incrementally.

Minimal viable capability involves capturing estimating assumptions in structured form at estimate creation, even if actuals are not yet being used systematically. This creates the foundation for future learning without requiring the full analytical infrastructure immediately. Key drivers, contextual factors, and critical assumptions are recorded consistently, establishing the baseline against which actuals will eventually be compared.

Initial learning capability adds periodic manual analysis of completed projects, mapping actuals back to assumptions for selected high-value projects or problem areas. This is resource-intensive and does not scale, but it builds organizational understanding of what learning from actuals requires and where the data gaps exist. It also produces early wins that demonstrate value and build support for further investment.

Systematic learning capability introduces repeatable processes and analytical tools that reduce the manual effort required to extract insights from actuals. Driver-level analysis becomes routine rather than exceptional. Statistical methods help identify patterns that are not obvious from individual project reviews. Models are updated on a regular cadence as new projects complete.

Advanced learning capability employs machine learning techniques, Bayesian updating, and hierarchical models to learn from partial and imperfect data across large portfolios. Learning occurs continuously rather than periodically. Insights are integrated directly into estimating tools and workflows, becoming embedded in standard practice rather than requiring separate analysis.

Most organizations will progress through these levels incrementally over several years. Attempting to jump directly to advanced capability without building foundational discipline typically results in sophisticated models that are not trusted or used because the organizational muscle memory for learning systematically has not been developed.

Critical Failure Modes to Avoid

Understanding how actuals-learning programs fail is as important as understanding how they succeed. Several failure modes recur with sufficient regularity to warrant explicit attention:

Model overconfidence from limited data: When models are built on small samples but present results with spurious precision, they create false confidence. Actuals from ten projects do not support the same level of inferential confidence as actuals from one hundred projects, but this distinction is often obscured in presentation. Uncertainty quantification must be honest and prominently displayed.

Learning from unrepresentative samples: Projects that complete successfully are more likely to have complete and well-organized actuals than projects that encounter significant problems or settle in dispute. If learning systematically excludes troubled projects, models inherit survivorship bias and will tend to underestimate risk.

Failure to detect model degradation: Cost drivers and their relationships change over time as delivery methods evolve, market conditions shift, and regulatory environments change. Models calibrated on historical data can become progressively less relevant without triggering obvious warnings. Regular validation against recent projects and explicit review of model assumptions are necessary to detect drift before it becomes problematic.

Treating learning as a one-time exercise: Organizations sometimes invest heavily in building initial models but fail to establish ongoing processes for maintenance and updates. Models become stale, trust erodes, and estimators revert to previous methods. Learning from actuals is not a project; it is an ongoing capability that requires sustained resourcing.

Ignoring feedback from estimators: When models produce results that conflict with experienced estimator judgment, both possibilities must be considered seriously. Sometimes the model has identified a genuine pattern that estimators had not perceived. Sometimes the model is wrong because data quality or sample composition created spurious relationships. Dismissing either estimator judgment or model output reflexively is a mistake. The most effective implementations establish structured processes for investigating and resolving such conflicts.

Making Learning Sustainable

Using actuals to improve estimating is not a one-time exercise. It is a capability that improves incrementally over years as organizational discipline develops, data coverage expands, and confidence grows. Early models will be crude and limited in scope. Insights will be partial and provisional. Over time, as more projects are delivered and more data becomes structured appropriately, relationships stabilise and the value of systematic learning becomes undeniable.

Modern analytical techniques make this process more tractable by reducing the manual effort required to extract insight from imperfect data and by making partial learning feasible when complete data is not available. They do not eliminate uncertainty or substitute for estimating expertise, but they help organizations understand cost behaviour more clearly and update their understanding systematically as new evidence emerges.

The real shift required is cultural rather than technical: treating estimating as a learning system rather than as a static function. When that shift occurs, actuals stop being an afterthought or a compliance exercise and become a strategic asset that compounds in value with each project delivered. The feedback loop that exists in theory can begin to function in practice, and estimating performance improves not through exhortation but through disciplined accumulation of evidence about what actually happens when projects are built.